If interest rates are lower than when you were initially given a loan, you may be able to save alot of money by refinancing. The question usually is, “Exactly how much might you be able to save?”

Mortgage rates were at all-time lows in early August, but began to rise last week because of a new adverse-market refinance fee of 0.5% that takes effect September 1st. So while refinancing today isn’t as attractive as it was at the start of the month, it might still be able to save you thousands of dollars.

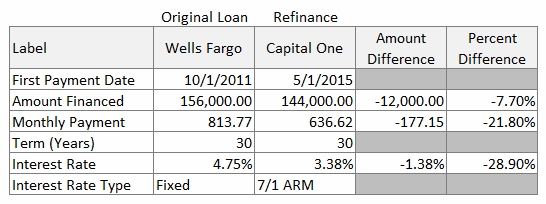

I’ve only refinanced once and that was about 5 years ago when it took my interest rate from 4.75% in 2011 for a 30-year fixed rate mortgage to 3.375% in 2015 for a 30-year adjustable rate mortgage:

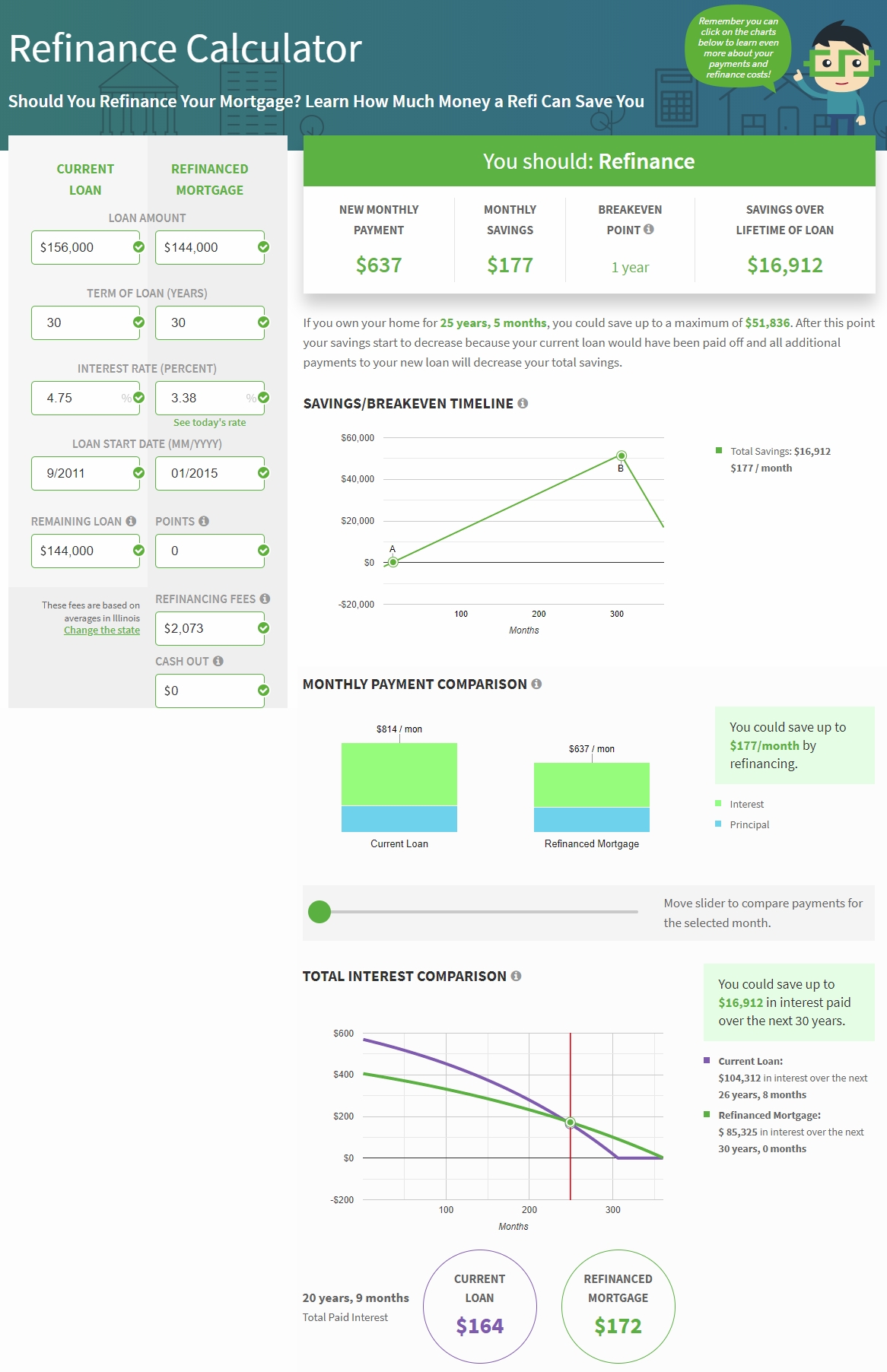

It took my monthly mortgage payment from $814/month to $637/month, or $177/month less which is $2,124/year cheaper. My closing costs were $2,074 so after about one year into my refinanced mortgage, I would begin saving money. MoneyGeek.com has a very simple refinance calculator that allows you to easily compare how much you would save by refinancing. The image below contains the MoneyGeek.com refinance calculations for my loan for reference:

According to the refinance calculator, if I stay in my current home until I payoff the refinanced mortgage in 2045 and the interest rate stays the same, I would save $16,912:

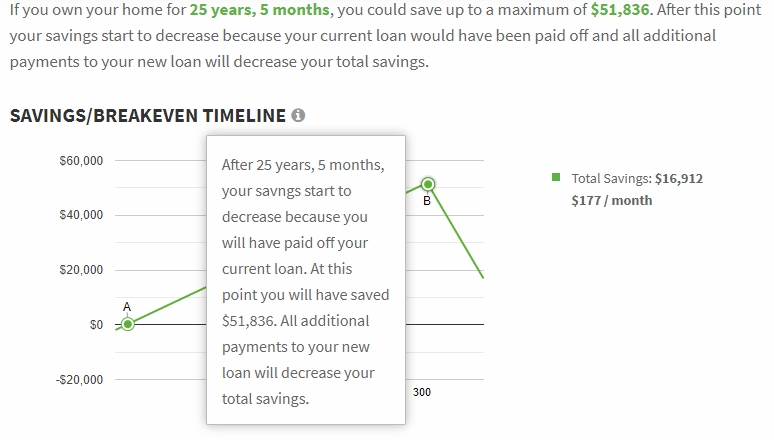

The refinance calculator shows that 25 years and 5 months into my refinanced mortgage (or around 2041), my refinance savings would hit a high of $51,836, but that would slowly start to drop because I would no longer be saving money at that point since my original loan 30-year loan from 2011 would have been paid off in 2041, so any mortgage payments made after 2041 just reduces the savings until it plateaus at $16,912 in total savings. (Note that if I wanted to maximize my gain and achieve the $51,836 of savings, I could try to completely pay off the remaining $25,000 mortgage balance I would have around 2041, but I would probably be too old or too rich to care by then.)

{kind=link}

{kind=link}

In reality, going from a fixed rate mortgage to an adjustable rate mortgage makes my actual savings impossible to predict, at least until the interest rate changes, but I wanted to quickly walk through the potential savings from refinancing assuming the refinance was with a fixed rate mortgage, which the vast majority of people refinance into.

I chose to refinance with an adjustable rate mortgage in 2015 because the interest rate was a little lower than a fixed rate mortgage but it can also be very risky because according the terms of the loan my interest rate can go as high as 8.375% when it adjusts in 2022 and my mortgage would jump from $637/month to $998/month. But the loan documents also state that the interest rate can go as low 2.25%, which would drop my mortgage by $87/month and make my mortgage payment $550/month if that were to happen.

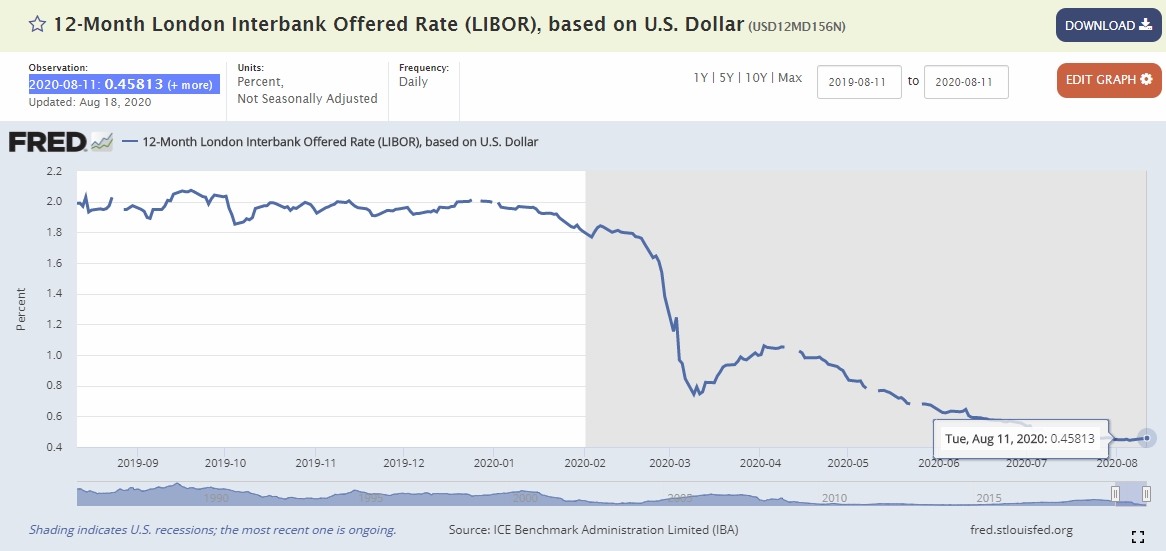

My interest rate is dependent on the 12-month LIBOR rate, which is currently about 0.45%:

Based on the adjustable rate terms in the loan documents, if my interest rate were to adjust today my interest rate would be about 2.7%, which is the 2.25% minimum rate plus the 0.45% LIBOR rate and that would make my mortgage payment $584/month. Who knows where interest rates will be when my rate adjusts in 2022, but my plan is to have my mortgage paid off before then.

There’s some work and a little math involved in trying to determine and understand how much money you can save by refinancing, but it’s not overly difficult. The MoneyGeek.com refinance calculator can provide a good estimate to help you figure out how beneficial refinancing may or may not be.

For the record, my savings from refinancing in 2015 all the way through when my rate adjusts in 2022 will be $12,807 over seven years, or $1,829/year. Take that to the bank.

{kind=link}