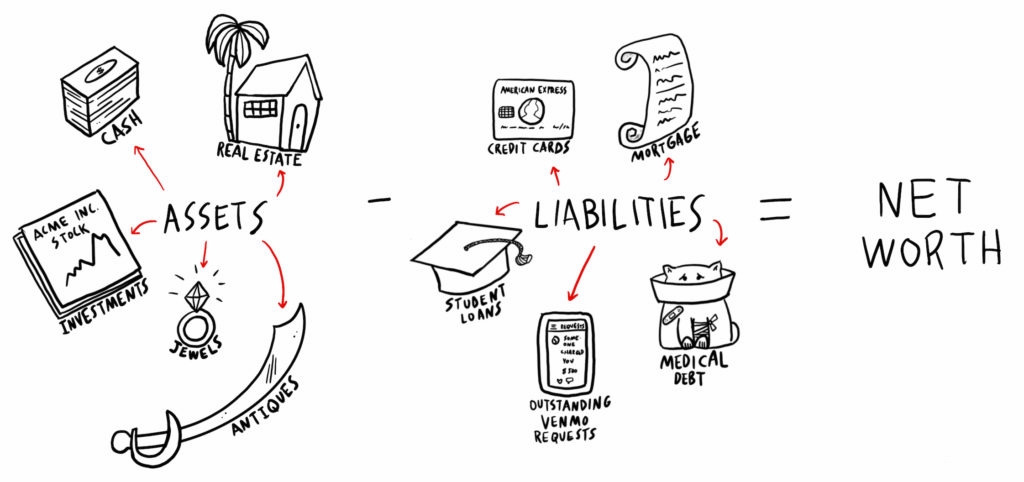

Net worth is the value of all the assets you own minus all the debt you have. According to an article from Business Insider last year, the net worth of the average millennial is about $8,000.

People born between 1980 and 1995 are typically considered millennials, which is my generational group, but there’s obviously a huge range in where millennials actually fall in that $8,000 average net worth. The table below from TheCollegeInvestor.com is a little more specific and estimates the average millennial net worth by age. The “Class of 20XX” label in parenthesis in the first column refers to the year most of the people in your age group, if you’re a millennial, graduated from a 4-year college.

It can be very unhealthy to compare yourself to others, but I think it’s very important to at least recognize where you financially stand compared to your peer group and to try to understand why that is. Not for the purpose of celebrating how much better you may be or to bemoan how much worse you are, but so that you can recognize what you may need to do to improve your finances if that’s important to you.

I was a bit of a late bloomer and didn’t graduate college until 2007. The estimated net worth today for people in my college group is $25,517. I haven’t done a real accurate calculation of my net worth, but looking at a spreadsheet I use to track my assets and liabilities, as of April 2021, I’m conservatively estimating that my net worth is approximately $200,000 or about 8 times higher than what’s listed in the table for my college graduating class. About half of my net worth comes from the equity in my home and investment property. The other half just comes from the $325,000 of assets I have in savings, brokerage and retirement accounts less the $225,000 in debt I have in home and car loans.

I’ve only tracked my assets and liabilities for a few years, but I’m estimating that my net worth in 2017 was as low as negative $100,000 with approximately $150,000 in assets and $250,000 in liabilities. My particularly high savings rate, the increased value of my real estate and retirement accounts, and the beginning of my wonderful wife’s full time employment in 2017 all drove the $300,000 increase in net worth between 2017 and 2021.

{kind=link}

The future is never certain, but God willing, if everything goes as planned, I think I should be able to achieve a net worth of a million dollars in ten years. I’m not sharing my goal in order to be admired. I’m sharing this information to gently light a fire under your arse and to encourage others to be elite with their money. Your financial capacity might not be the same as mine, and my financial capacity may never be the same as a CEO of a fortune 500 company, but based on the lifetime earnings of the average worker in the United States ($1,344,680 lifetime earnings over a 40-year career or $33,617/year), it’s hard for me to see how the average American, so long as they don’t start too late, can’t eventually become financially independent1, especially if they are wise and careful with their money. Even more so if they have a dual income household.

Besides winning the lottery or having rich parents, the most important factor in reaching financial independence is your savings rate, which is just the difference between how much you earn and how much you spend. It’s hard to have a really high savings rate without a high income, but a high income isn’t a requirement for financial independence, it just helps you get there faster.

If you’re a millennial or younger who has trouble controlling their spending or is bad with money, or even if you’re someone who’s already better than average or makes a great salary, realize that you can greatly influence how soon you achieve financial independence by living modestly, not buying the newest iPhone every year, purchasing a used car instead of a brand new car, buying a modest house instead of a high-end home and making many other frugal and prudent financial choices.

The sooner you pursue financial independence, if that’s something that matters to you, the less daunting the road becomes.